r/oil

▲ 61 r/oil

There is no good outcome for this oil crisis

These are the options:

Escalate conflict to force open the straits and more energy infra may get destroyed, to the point opening the straits would be less useful. And this may drag on a few months. This would drain US ammos which are already heavily depleted leaving not much for self-defense .

cave in to Iran’s demands but that would be a big humiliation and Iran will control the straits and charge tolls . Accomplished nothing but gave iran everything. The end of pax Americana which a big deal similar to the suez canal crisis. Also Gulf states won’t accept iran controlling the straits?

stalemale for another 1-2 months: time is ticking, fuel shortage, rising inflation and oil price, rising bond yields (already in danger territory), recession risk rises

iran economy collapses within 2 months, this may or may not be a miscalculation , but as noted by a commenter, iran may continue to fight when economy collapses. They may bring down the entire world as a last resort

peace deal (both sides compromise): seems unlikely though, they have been negotiating for 2 months but made absolutely no progress

It really seems the first 3 options are more likely . But 1 and 3 would result in a market crash. Option 2 would save the economy but it is admitting defeat (plus Gulf states which are US allies may not accept)

What do y’all think?

u/SadComparison9352 — 4 hours ago

▲ 48 r/oil

Two Chinese supertankers, carrying 4M barrels of Middle East crude, heading to Guangdong and Fujian

Two Chinese supertankers, laden with a total of 4 million barrels of Middle Eastern crude oil, departed on Wednesday. Their exit followed a wait of over two months in the Gulf.

These vessels are part of a small group of supertankers transporting Iraqi crude oil out of the Gulf this month. This movement is occurring via a transit route mandated by Iran.

The Chinese-flagged Very Large Crude Carrier (VLCC) Yuan Gui Yang loaded 2 million barrels of Iraqi Basrah crude on February 27, shortly before the outbreak of the U.S.-Israeli tensions involving Iran, according to the data. Chartered by Unipec, the trading division of Sinopec, Asia’s largest refiner, the ship is projected to arrive at Shuidong Port, near Maoming city in southern Guangdong province, on June 4 to unload its cargo.

The Hong Kong-flagged VLCC Ocean Lily, owned by Chinese firm Sinochem, took on 1 million barrels each of Qatari al-Shaheen and Iraqi Basrah crude between late February and early March, the data indicates. It is expected to arrive at Quanzhou Port in eastern Fujian province on June 5 for cargo discharge.

Sinopec, Sinochem, and Cosco Shipping, which own and manage the Yuan Gui Yang, have not yet provided comments. Last week, the VLCC Yuan Hua Hu also exited the strait, carrying 2 million barrels of Iraqi oil and destined for Zhoushan Port in eastern China.

u/StarFEU-Commodity — 7 hours ago

▲ 260 r/oil

Southeast Asia Is Getting Crushed By the Hormuz Crisis. Here's What the Data Says Is Coming.

Glossary and Sources with Links at the bottom. Please let me know if there are mistakes or anything else I can do to improve it.

TLDR (Brief Summary)

The Strait of Hormuz has been closed for 80 days.

The numbers that matter:

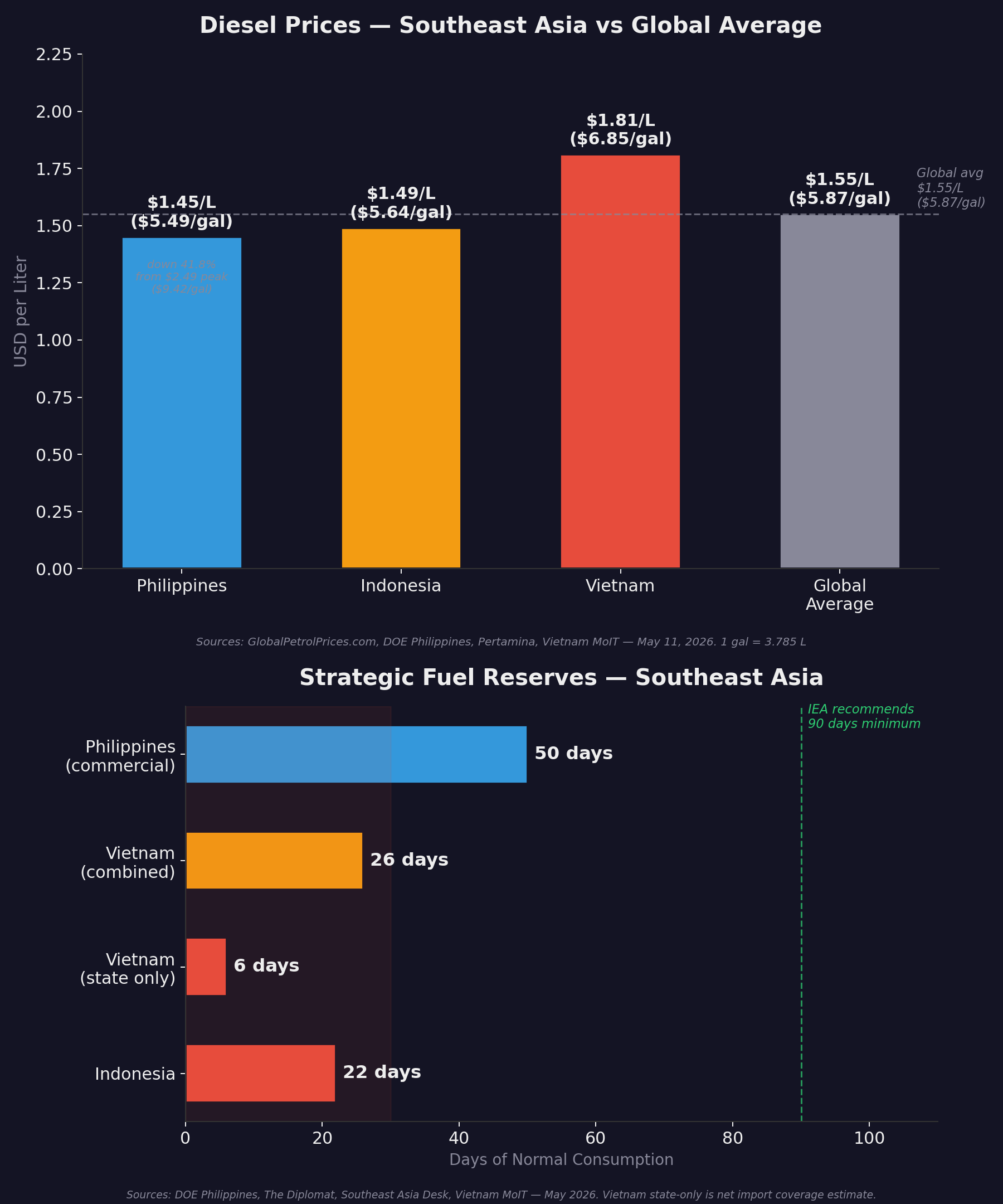

• Philippines: Diesel hit $2.49/L ($9.42/gal) in April before government crashed it to $1.45/L ($5.49/gal). Still +58% from three months ago. 400+ filling stations closed. 2 million people facing brownouts. First SEA country to declare a national energy emergency.

• Indonesia: Diesel at all-time high $1.49/L ($5.64/gal, +88% YoY). Only 21-23 days of reserves, the lowest in the region. 65 million households cook with LPG, 70% imported. Rationing already live: 50L/day cap for private vehicles.

• Vietnam: Best position with two domestic refineries covering ~68% of demand, but diesel at $1.81/L ($6.85/gal), above the global average. State reserves just 5-7 days of net imports.

The Singapore blind spot: Singapore is the region's refining hub. If Middle Eastern crude stops flowing to Singapore, every country that buys Singaporean diesel (Philippines, Indonesia, Vietnam) loses supply simultaneously.

Shipping collapse: Hormuz went from 70-80 vessels/day to single digits. 20 million barrels/day collapsed to near zero. Rerouting around Africa adds 10-20 days transit. Freight rates +29%. LNG spot +140%. GPS jamming affects 1,600+ vessels.

The archipelago problem: The Philippines (7,641 islands) and Indonesia (17,000+ islands) have fuel distribution that burns fuel. Every liter of diesel burned on an inter-island ferry is a liter that doesn't reach a fishing boat or a generator. Islands at the end of the chain get hit first, where poverty is deepest.

Fertilizer squeeze: The Persian Gulf supplies over 30% of global urea and 45% of global sulfur. Southeast Asia's rice farmers are now competing with the world for a shrinking fertilizer supply at prices smallholders cannot absorb.

Scenarios: Best case, Strait reopens by early June, oil drops to $70-75, recovery begins Q3. If closed through summer, oil $100-130, Indonesia hits tank bottoms late May to early June, 5-10 million below poverty by August. Worst case, closed through 2026, oil $150+, subsidy systems collapse, deep global recession.

Malaysia is a net exporter with its own production, serving as a critical fuel lifeline to its neighbors.

(End of Summary/ TLDR)

Charts:

Diesel prices and strategic fuel reserves across Southeast Asia:

{kind=link}

Diesel prices shown per liter and per gallon. Sources: GlobalPetrolPrices.com, DOE Philippines, Pertamina, Vietnam MoIT, The Diplomat, Southeast Asia Desk. May 2026.

Note: Fuel prices and reserve figures draw from national regulators and press reports during a fast moving crisis. Specific prices may shift day to day. Where possible, verification dates are noted. All claims are cited; some sources are data portals where specific pages change. This is analysis, not investment advice.

The Strait of Hormuz has been closed for 80 days as of May 19, 2026. Nearly 20% of the world's oil trade normally transits Hormuz, and with the Strait closed, the IEA calls this "the largest supply disruption in the history of the global oil market," larger than the 1973 oil shock that created the IEA itself.

Global diesel: $1.55/L ($5.87/gal) average.

The Singapore blind spot: Singapore is Southeast Asia's refining powerhouse.

It imports Middle Eastern crude and exports the diesel, gasoline, and jet fuel that the Philippines, Indonesia, and Vietnam buy.

If the Strait stays closed, Singapore's refineries run dry.

The whole region loses its gas station at once, long before individual countries hit their tank bottoms.

The shipping collapse makes it worse. Before the war, 70 to 80 vessels transited Hormuz daily.

By the second week of March, that number was in single digits.

Crude and product flows through the Strait collapsed from roughly 20 million barrels per day to a near standstill; the IEA now describes the resumption of flows through the Strait as "of paramount importance for the oil market."

Ships now reroute around the Cape of Good Hope, adding 10 to 20 days of transit time per voyage.

Freight rates on Far East to US routes jumped 29%.

Asian LNG spot prices spiked 140%.

Singapore and Malaysia's Port Klang are both reporting severe congestion as redirected vessels overwhelm port capacity.

The IRGC imposed tolls of up to $2 million per ship for passage through the Strait. War-risk insurers pulled coverage.

GPS jamming in the Gulf now affects over 1,600 vessels.

Philippines: First To Crack

The Philippines imports 98% of its crude oil. The transport sector consumes nearly two-thirds of all petroleum used in the country. FIRST in Southeast Asia to declare a national energy emergency (March 24).

- Diesel hit an all-time high of PHP 153.70 ($2.49/L, $9.42/gal) on April 13. Government intervention crashed it to PHP 89.50 ($1.45/L, $5.49/gal) by May 11, but still +58% from three months ago.

- Gasoline: PHP 134.50 ($2.17/L, $8.21/gal), well above the $1.51/L ($5.72/gal) global average.

Over 400 filling stations closed. Logistics rates jumped 30% as diesel surged. Brownouts hit nearly 2 million people in mid-May as power plants ran dry.

- The Philippine Institute for Development Studies estimates 1.3 to 3.1 million Filipinos could fall into poverty.

- A transport strike shut down Manila for two days.

- Fuel reserves dropped from 55-57 days to 45 days by March 20, but recovered to 51 days by March 27 and 54 days by late April after aggressive procurement.

- LPG stocks were ~24 days in late March. The Philippines imports roughly 80% of its LPG from the Middle East.

Government measures: 20B pesos from the Malampaya gas fund for fuel procurement. 20B pesos in subsidies to ~300K transport workers. LPG and kerosene excises removed (RA 12316). 329K barrels of diesel procured from Malaysia, 700K barrels from Russia under US sanctions waiver. Cebu Pacific and Philippine Airlines suspended routes to conserve fuel. Schools shifted to flexible learning. Malls cut operating hours.

Indonesia: All-Time Highs, Razor-Thin Reserves

Indonesia produces some of its own oil but hasn't built a major refinery in decades. It imports ~63% of its refined fuel and ~70% of its LPG. Strategic reserves: just 21-23 days, among the lowest in the region.

- Diesel: IDR 26,000/L ($1.49/L, $5.64/gal). ALL-TIME HIGH. +77.8% month-over-month, +88.3% year-over-year.

- A 40L tank costs 8.1% of monthly income at the average; the poorest pay a far bigger share.

- Gasoline remains subsidized at $1.20/L ($4.54/gal), masking the real price.

Prabowo moved fast: capped fuel prices, and secured LNG and oil deals with Japan, South Korea, and Russia (Indonesia also has a February trade agreement with the US obligating ~$15B/year in US energy imports).

On the biodiesel front, he went further: the B40 mandate (40% palm oil blend) was already cutting diesel imports. In late March, during a visit to Japan, Prabowo reinstated the B50 mandate, a 50% blend that had been scrapped in January due to technical and funding concerns.

The Hormuz crisis made aggressive diesel substitution an urgent national priority. B50 demands an additional 2.2 to 2.3 million tons of crude palm oil per year, diverting roughly 8% of Indonesia's palm oil export volume (or about 4-5% of total production) into fuel tanks, on top of what B40 already consumes.

However, only three of the five large-scale processing plants required are currently under construction, so implementation faces serious bottlenecks.

Rationing is already live. Starting April 1, subsidized fuel purchases are capped at 50 liters per day for private vehicles, 80L for public transport, 200L for large trucks under BPH Migas Decree No. 024/2026, enforced via the MyPertamina digital system.

The price gap between subsidized and non-subsidized diesel is over Rp 16,800/L ($0.96/L, $3.63/gal), a cliff that destroys margins for any fleet that exceeds its cap.

But you can't close a 63% import gap overnight. 65 million households cook with LPG. Analysts project tank bottoms could hit between late May and early June; if so, Indonesia faces deeper rationing or ruinous subsidy spending.

Vietnam: The Best Buffer, Still Bleeding

Vietnam has the best position: two domestic refineries (Dung Quat and Nghi Son) cover ~68% of demand, plus its own crude production.

- Diesel: VND 44,500/L ($1.81/L, $6.85/gal), significantly above the $1.55/L ($5.87/gal) global average.

- Fuel reserves increased to 26 days (up from 15 before the crisis), according to Minister of Industry and Trade Le Manh Hung. The government plans further increases.

- Vietnam's plan to procure 4 million barrels of non-Middle Eastern crude equals roughly six days of consumption, useful buffer, not a solution.

- Vietnam cut fuel taxes, activated price stabilization funds, and cut import tariffs to zero for non-FTA partners.

- Vietnam imports ~70% of its crude from the Middle East, a dependency the government is now racing to diversify.

The food multiplier: Vietnam is the world's third-largest rice exporter. If the strait stays closed through planting season, fertilizer costs spike and rice yields drop. The Persian Gulf supplies over 30% of global urea, the nitrogen fertilizer that Vietnam's rice paddies depend on. The Philippines and Indonesia are major buyers of Vietnamese rice. When fuel and fertilizer both spike at the same time, food and fuel shortages compound.

The Archipelago Problem

The Philippines (7,641 islands) and Indonesia (17,000+ islands) face brutal arithmetic no land-based country deals with: fuel distribution burns fuel. Every liter of diesel burned on an inter-island ferry is a liter that doesn't reach a fishing boat or a generator. Islands at the end of the chain (Palawan, Maluku, Eastern Visayas, Papua) get hit first and hardest, exactly where poverty is deepest.

When ships can't get diesel, the supply chain for everything breaks. This happens during typhoons locally. In this scenario, it would be national and prolonged.

Hidden Ripple Effects

- Singapore Dries Up: SEA's refining hub relies on Middle Eastern crude. If Singapore stops refining, every country that buys its fuel (Philippines, Indonesia, Vietnam) loses supply simultaneously. National reserve numbers stop mattering when the regional gas station is empty. Port congestion from redirected vessels is already a problem.

- B50 = Cooking Oil Pressure: Indonesia's reinstated B50 biodiesel mandate (50% palm oil in diesel) diverts an additional 2.2 to 2.3 million tons of crude palm oil per year into fuel tanks. Indonesia produces ~60% of global palm oil. The mandate is active. Global cooking oil prices face sustained upward pressure, hitting developing countries that import palm oil for food the hardest.

- The Coal Threat: The Philippines relies on Indonesian coal for baseload power (~85% of coal imports). If Indonesia restricts coal exports to secure its own grid in a panic, the Philippine grid goes dark, not brownouts, blackouts.

- Malaysia: Malaysia is a net oil and gas exporter with its own production, serving as a critical fuel lifeline to its neighbors (Philippines has already procured diesel from Malaysia).

- The Fertilizer Squeeze: The Gulf supplies 45% of global sulfur and over 30% of global urea. Sulfur is essential for phosphate fertilizer production. Urea is the most widely used nitrogen fertilizer on the planet. Southeast Asia's rice farmers are now competing with the world for a shrinking fertilizer supply, at prices that smallholders cannot absorb.

- Regional Inflation Already Spiking: Thailand's inflation hit 2.89% in April 2026, driven directly by the oil price surge. The Asian Development Bank projects 3.2% inflation for Southeast Asia in 2026.

Scenarios

Best case: Strait reopens by early June, oil drops to $70-75. The ~400 million barrels of emergency reserves released by the IEA bought enough time for most countries to avoid tank bottoms. Philippines keeps its refilled reserves above 50 days. Indonesia's rationing eases by July. Recovery begins in Q3.

If the strait stays closed through summer: Oil $100-130. Indonesia hits tank bottoms late May to early June; rationing deepens. Philippines burns through its recovered reserves if Singapore's refineries go dry. Vietnam holds at 26 days but faces diesel prices well above the global average. By August: 5-10 million below poverty, GDP near zero for the Philippines.

Worst case: Closed through 2026, oil $150+. Subsidy systems collapse. Islands lose deliveries. Inflation 15-20%. The archipelago supply chain breaks. Deep global recession.

What Can Be Done

Governments: Ration by priority sector BEFORE reserves hit tank bottoms. Secure LPG from alternative sources. Cash to transport workers, not fuel subsidies (those subsidize SUV owners). Prioritize fuel for inter-island cargo vessels. Build strategic reserves to 90 days minimum.

Families: Consolidate errands, share rides. If LPG runs short, cook with wood or charcoal outdoors. Community cooking saves fuel. Root vegetables store longer and need less fuel. Form mutual aid networks for shared fuel runs and bulk purchases.

If you're in Southeast Asia, what are you seeing on the ground that matches or contradicts any of this? Also thank you guys so much for my the words of encouragement and positive support! Truly appreciate it. Just share, cross post, give me an upvote and credit!

Glossary

Hormuz: Strait between Iran and Oman. ~20% of global oil transits here. Closed since Feb 28, 2026.

Tank bottoms: Minimum operating level of a fuel storage tank. Below this (~10-15% of capacity), pumps fail and distribution stops.

LPG: Liquefied petroleum gas (propane/butane). Primary cooking fuel for hundreds of millions of households in Asia.

Strategic reserves: Government-held or mandated commercial oil/fuel stocks, measured in days of normal consumption. IEA recommends 90 days minimum.

B50 biodiesel: Indonesia's mandate blending 50% palm oil biodiesel with 50% conventional diesel. Reduces diesel imports but competes with food/cooking oil supply.

Brent crude: The global benchmark price for oil. ~$109/barrel as of mid-May 2026.

Jeepney: Philippine minibus (converted military jeep). The country's most common public transport. Runs on diesel.

Cape of Good Hope: Southern tip of Africa. The alternate shipping route when Hormuz/Suez are closed. Adds 10-20 days transit time.

OFW: Overseas Filipino Worker. Remittances from OFWs are a major pillar of the Philippine economy.

Pertamina: Indonesia's state-owned oil and gas company. Controls fuel pricing and LPG distribution.

Dung Quat / Nghi Son: Vietnam's two domestic oil refineries, covering ~68% of demand.

Key sources:

IEA Sheltering From Oil Shocks report March 2026 ("largest supply disruption in the history of the global oil market")

IEA Oil Market Report March 2026

GlobalPetrolPrices.com (live diesel/gasoline, verified May 11 vs national regulators)

VietNamNet (Minister Le Manh Hung on 26-day reserves, Apr 10 2026)

EezyImport (Hormuz shipping collapse, freight rate data, port congestion, GPS jamming)

CNBC (Fatih Birol interview, Mar 23 2026)

Rappler / PhilStar / DOE (Philippine reserve levels)

Tempo.co / CNBC Indonesia (MyPertamina rationing)

Straits Times (Prabowo B50 reinstatement, Mar 30 2026)

UkrAgroConsult (B50 requires 2.2-2.3M tons additional CPO)

Advanced BioFuels USA (only 3 of 5 B50 plants under construction)

Xinhua (Thailand April 2026 inflation 2.89%, cites Trade Policy and Strategy Office)

ADB (projects 3.2% SEA inflation 2026)

Lowy Institute (Philippines energy dependency), IEEFA, The Diplomat, The Guardian

Archive links:

u/alemorg — 13 hours ago

▲ 162 r/oil

Is Trump’s stop-start Iran strategy making the Strait of Hormuz crisis worse for oil markets, or is delaying strikes the only realistic way to avoid a bigger supply shock?

americareport.usu/bauernebel — 16 hours ago

Dwindling US Distillate inventory (Diesel)

Distillate stocks have fallen to ~102 million barrels as of 8-May from ~119 in early March. New EIA report will be out tomorrow for fresh status as of 15 May.

100 mb is the danger level as per Currie, and essentially we are there already. Things will get worse end of May and early June. Currently, US is drawing inventory at rate of 7-10mb per month. Things get very ugly June onwards because the inventory cannot be drawn to 0, 25 mb of the 102 is unusable. 90-100 mb is the number below which regional shortages will begin.

Some sort of export controls by the US are not out of the question.

u/Independent-Ruin926 — 18 hours ago

▲ 235 r/oil

The oil crisis is so bad in Kenya that protesters have lit bonfires in the middle of Nairobi

Protests erupted in Kenya’s capital Nairobi Monday as a nationwide public transport strike kicked off in protest at rising fuel prices.

Commuters were stranded in various suburbs and the city center remained deserted. Drivers with private vehicles opted to stay home as protesters burned tires on major roads.

The Kenya Association of Private Schools had advised its members to assess the safety of students going to school, and most schools opted for online learning.

Kenya’s fuel prices hit a record high on Friday with the diesel price increasing by 23.5% and gasoline by 8%.

President William Ruto, who has been out of the country, is yet to comment on the new prices. In the last price review in April he attributed it to the Iran war but reduced the taxes to prevent a sharp increase in price at the time.

Read more [paywall removed for Redditors]: https://fortune.com/2026/05/18/the-oil-crisis-is-so-bad-in-kenya-that-protesters-have-lit-bonfires-in-the-middle-of-nairobi/?utm_source=reddit/

u/fortune — 19 hours ago

▲ 3 r/oil

DAILY MEGATHREAD May 19, 2026 : US Blockade of the Strait of Hormuz is LIVE – All tanker drama, oil panic, missile hits, Iran retaliation posts belong HERE

This is posted daily at 9 am AUET

This is the one official Hormuz Blockade Daily Megathread for {{date %B %d, %Y}}

Is it open yet: https://www.ishormuzopenyet.com/

Everything else gets yeeted into the void (or at least politely redirected here). New articles, memes, wild speculation, questions about how screwed your superannuation is, grainy satellite pics of tankers doing U-turns — drop it all below.

Quick rules so we don’t sink this thread too:

- Be civil. This isn’t Twitter.

- Actual sources or at least say “saw it on twitter” so we know how cooked it is.

We’re all watching the same slow-motion geopolitical car crash anyway — might as well watch it from one thread instead of 47 identical ones.

- What’s the latest you’ve seen?

- Any tankers actually turned around yet?

- Oil price predictions?

- Or are we all just doom-scrolling until someone blinks

Overview on Iran and the situation: https://www.iransitrep.com/

Feel free to report this post as low effort / AI slop that it is. We'll be sure to take it under consideration

u/AutoModerator — 10 hours ago

▲ 99 r/oil

Oil prices fall as Trump postpones Iran strike, easing supply disruption fears

cnbc.comu/Ayox_Gur1244 — 23 hours ago

▲ 4 r/oil

Daily Oil Price Opinions - May 19, 2026 All other Oil Price Posts Will Be Removed

What are your thoughts on today’s oil price? Drop your opinions, predictions, charts, memes , low and high effort post, your AI slop or even analysis below. Keep it civil and on-topic! This post is renewed daily.

Unless there is some compelling reason, other posts in the sub about oil prices will be removed. In a futile effort to improve the quality.

(Current WTI/Brent price can be checked on any major site.)

u/AutoModerator — 22 hours ago

▲ 467 r/oil

Jet fuel: the West Coast USA (PADD5) will experience jet fuel shortages in early June, rationing in late June and systemic collapse in early July, based on forecast production, import and consumption rates

u/MarmotFullofWoe — 1 day ago

▲ 837 r/oil

Iran formalizes Strait of Hormuz control and toll collection

This should speed things along nicely..

u/i_like_cake_96 — 1 day ago

▲ 8 r/oil

Doomberg: The Strait of Hormuz is Closed — What It Means for Canadian Pipelines

Doomberg thinks Middle East producers are getting ~ 10M bbl/day out of the area, including Iran shipping significant volumes to China.

u/yycTechGuy — 19 hours ago

▲ 533 r/oil

Oil markets could be a month away from the moment of truth. Brace for a "non-linear" price spike and panic buying, analysts warn

Dire warnings about oil supplies are coming from everywhere lately as the Strait of Hormuz remains largely closed while President Donald Trump’s trip to China failed to produce a breakthrough to reopen the critical waterway.

While investors have been trading on hopes that the Iran ceasefire will remain intact, there is little sign that the oil trade will return to normal soon, forcing them to reckon with the reality of worsening shortages and an imminent tipping point ahead.

JPMorgan predicted that commercial oil inventories in the developed world could “approach operational stress levels” by early June. Saudi Aramco said global inventories of gasoline and jet fuel could reach “critically low levels” ahead of the summer.

The International Energy Agency warned the world is drawing down oil inventories at a record pace, with 164 million barrels released by governments and industry as of May 8.

“Rapidly shrinking buffers amid continued disruptions may herald future price spikes ahead,” IEA said in its lately monthly report.

The U.S. and Israel launched their war on Iran two and a half months ago, and analysts expected the Strait of Hormuz to reopen by the end of May or early June.

Read more [paywall removed for Redditors]: https://fortune.com/2026/05/16/oil-markets-crude-non-linear-price-spike-panic-buying-inventories-iran-hormuz/?utm_source=reddit/

u/fortune — 1 day ago

▲ 15 r/oil

The offshore drilling trade picking up is a signal for oil being priced in higher for longer

Institutions seem to be increasing exposure to offshore drilling with RIG

{kind=link}

RIG added $1.6B of backlog in Q1, bringing total backlog to about $7.1B. That about a 29% increase.

Exposure from the options market is also growing on higher strikes

{kind=link}

NE, whichs is the other stock with notable flow added about $565M of new contract value, bringing backlog to around $7.5B -an 8% increase.

Higher for longer is being priced in.

Positioning on USO is building on $160 as well

{kind=link}

u/Smart_Money_HQ — 23 hours ago